Understanding the Unique Investment Needs of Women - Part 2

Navigating the Financial Challenges that Women Face

More women today are taking control of their financial futures.

But with this empowerment comes a new set of challenges that can quietly undermine long-term financial security.

Living longer, taking career breaks, and battling the gender pay gap aren’t just statistics on a page — they are real hurdles that require thoughtful planning and bold strategies. How can women turn these obstacles into opportunities for building lasting wealth?

This is the second instalment of the series and we’ll dive deeper into the financial hurdles that women face and explore strategies that can help them build stronger, more resilient financial futures.

Please help us grow by liking this post and sharing it with a woman you know! It really helps a lot :)

1. The Longevity Challenge

Women in Europe, on average, live longer than men. While this longevity is certainly a blessing, it also presents a significant financial challenge. According to Eurostat, women in the EU typically outlive men by about 5.5 years. Living longer means needing more savings to cover those additional years in retirement. With rising healthcare costs and the potential need for long-term care, women need to ensure their financial plans are set up to last the distance.

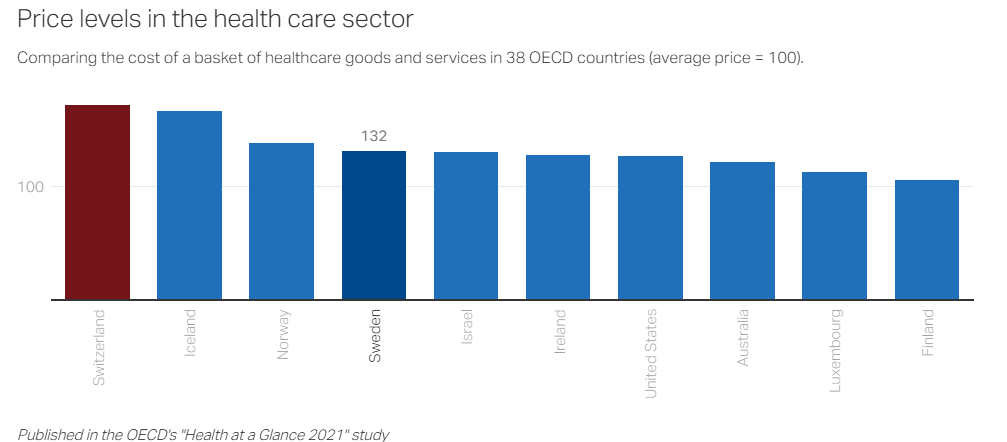

Take my adopted home Switzerland as a case in point.

Switzerland has the most expensive healthcare of the 38 Organisation for Economic Co-operation and Development (OECD) member states1

For many years, basic healthcare costs have risen above inflation.

In terms of cost contribution, residents spend more on healthcare costs in Switzerland than in any other country. It is little wonder that healthcare costs are often found among the top issues that the Swiss worry about.

This reality makes it crucial for women to invest wisely and plan aggressively for retirement. In Switzerland’s three-pillar pension system, ensuring adequate contributions to the second and third pillars (company pensions and private savings) is vital.

Strategy: Start saving early and consider longevity-focused financial products. For example, in Switzerland, consider maximizing contributions to your 3rd pillar pension, which offers tax benefits and flexibility. In the EU, explore pan-European personal pension products (PEPPs) when they become available in your country.

2. Career Interruptions and Part-Time Work

For many women, career interruptions are inevitable. Whether it’s for maternity leave, caring for aging parents, or other family responsibilities, these breaks can severely impact long-term earning potential.

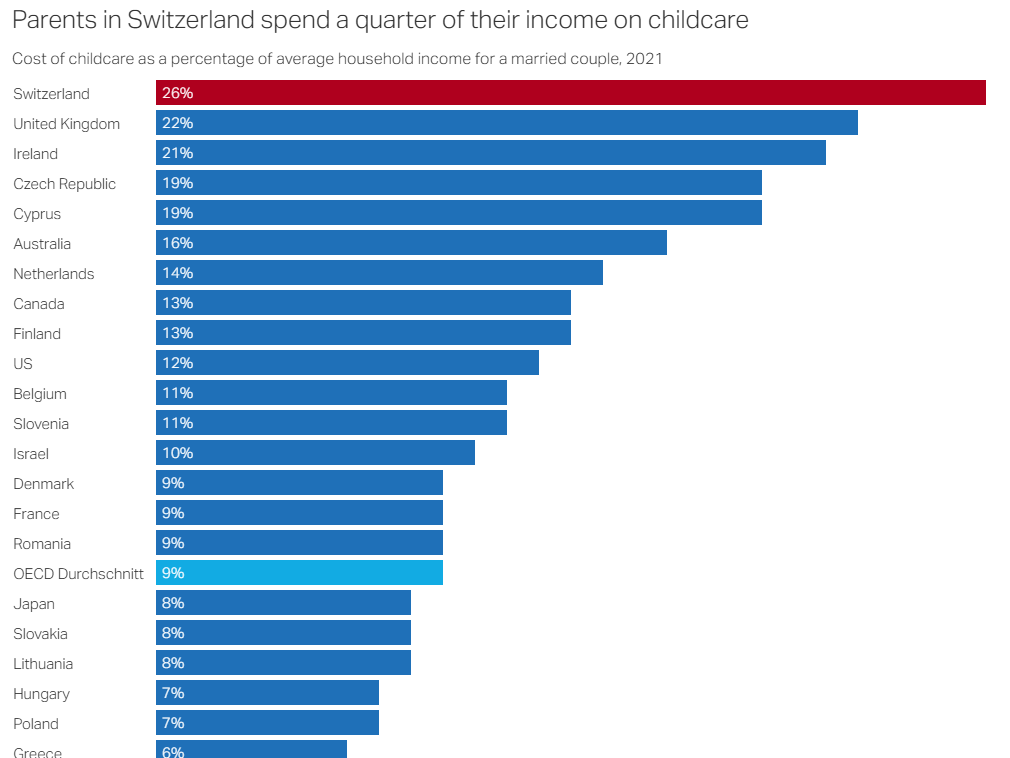

Take childcare as a case in point.

When it comes to professional childcare, Switzerland ranks as the most expensive of all the countries of the Organisation for Economic and Cooperation and Development (OECD).

The cost of bringing up two children in Switzerland is reason enough to give up on gainful employment. For most couples, the choice to give up on employment, or take up part-time employment sadly falls on the woman.

This so-called "child penalty" can still be felt even after the kids have grown up. This is because the years mothers spend raising their kids often hurt their career progression, salary, and retirement benefits in the years after they retire.

This penalty reduces the amount saved for retirement and can slow career progression, making it even harder to close the wealth gap later in life.

Planning for these interruptions is key.

Strategy: Women should explore ways to maintain pension contributions even during part-time work or career breaks, such as through voluntary contributions to the third pillar (tax-advantaged private savings).

They can also consider ways to keep their skills sharp during time away from the workforce, increasing the chances of re-entering at a higher salary level when they’re ready. I know friends who served voluntarily on advisory boards and committees to maintain marketable skills during those career breaks.

3. The Persistent Gender Pay Gap

Despite progress in gender equality, the gender pay gap remains a major issue in Europe. On average, women in the EU earn about 13% less than their male counterparts for the same work. Over a lifetime, this difference can snowball into significantly less wealth, smaller pensions, and greater financial insecurity in retirement.

Closing this gap starts with advocating for equal pay, but it doesn’t stop there. Women need to be proactive about their financial health, negotiating for higher salaries, pursuing higher-paying roles, and optimizing their investments.

As Wies Bratby, founder of Women in Negotiation, observes, “I’ve often seen talented women work twice as hard as their male counterparts, only to receive fewer promotions, less respect, and significantly lower salaries.” Many have accepted this reality because they either lack the confidence or the knowledge to proactively manage and negotiate their careers.

The tide is changing….slowly.

Pursuing higher paying roles, negotiating higher salaries and understanding the power of long-term investing & compounding returns is critical to counteracting the pay gap’s effects.

Strategy: Negotiate salaries aggressively, seek employers with strong equality policies, and consider additional income streams or side hustles.

4. The Global Pension Puzzle

For women who navigate international careers, the global pension puzzle adds a new layer of complexity.

Take my friend who I’ll call Lisa as a case in point.

Lisa is a 45-year-old marketing executive who, like me, has had an international career. She recently returned to Switzerland after a successful career stint spanning the United States, Singapore, and the United Kingdom. While her global experience was invaluable, it has left her with pension savings across multiple countries, each with its own set of rules.

Like Lisa, women with international careers often face fragmented pension landscapes, difficulty tracking multiple pension accounts, currency exchange risks, and complications with international tax treaties.

Upon returning to Switzerland, Lisa realized she had gaps in her Swiss pension contributions, potentially impacting her future state pension (AHV/AVS), occupational pension benefits (2nd pillar), and her ability to maximize tax-deductible contributions to the 3rd pillar.

Women in similar situations must navigate these complexities carefully to secure their financial futures.

Strategy:

Make voluntary contributions to the AHV/AVS (or the equivalent state pension scheme) to fill any gaps caused by time spent abroad. Consider “buy-ins” to the 2nd pillar pension to boost retirement savings and reduce taxes.

Work with an investment advisor experienced in cross-border wealth management who can help develop a cohesive global investment strategy, which might include currency hedging and leveraging international tax treaties for tax-efficient investments.

Turning Challenges into Opportunities

The financial challenges women face are undeniable—but they’re not insurmountable. Whether it’s tackling the longevity challenge, planning for career interruptions, addressing the gender pay gap, or navigating the complexities of an international career, the key is proactive, personalized financial planning.

By taking control of these hurdles, we can not only secure our financial futures but also turn these challenges into opportunities for building lasting wealth.

With the right strategies in place, women can ensure that their financial empowerment is not just about rewriting the rules, but about reshaping their futures for the better.

Disclaimer

The content in this newsletter is for informational purposes only and does not constitute financial, investment, legal, or medical advice. Opinions expressed are those of the author and may not reflect the views of affiliated organisations. Readers should seek professional advice tailored to their individual circumstances before making decisions. Investing involves risk, including potential loss of principal. Past performance does not guarantee future results.

Health at a Glance 2021 comparative study