The Weekly Market Compass #7

Santa's rally is here...or is it?

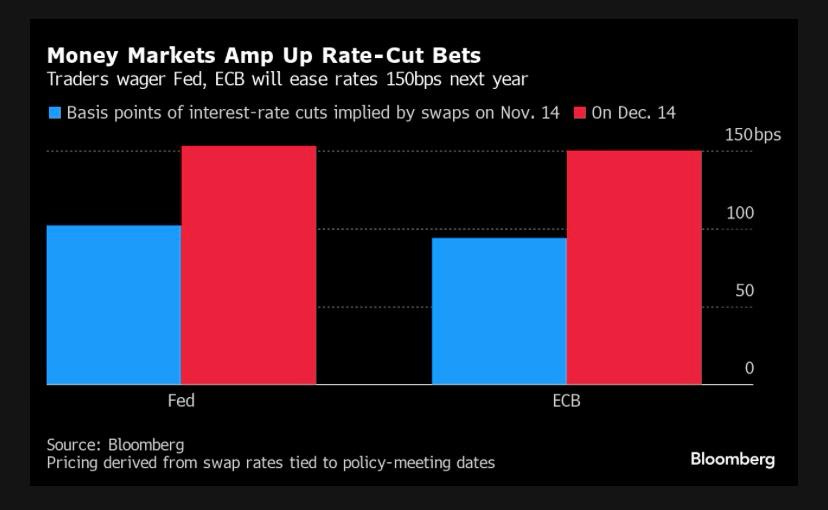

In a LinkedIn post last week, I wrote about the divergence between the Fed and the market expectations for rates using the dot plots as a case-in-point. And last week, well…the Fed pivoted.

The Fed pivoted from guiding the markets to being guided by the markets. And by markets, I am referring to the bond markets. Suddenly, the much-touted "higher-for-longer" stance vanished into thin air. The FOMC’s infamous dots now indicate expectations for a series of rate cuts next year.

And this is not just about the Fed. Everyone's starting to realize things aren't quite as they seem. Take China as a case-in-point. The PBOC has been aggressively injecting liquidity into the system. But so far, its not making much of the desired impact.

Looking at all these signs, it feels like we're on the cusp of something new.

So what’s really happening here?

Lets look at the bond markets to unpack what’s happening. At the time of writing the US 10Y (which a few weeks ago was hitting highs of 5%) is now below 4%. And even the US30Y long bond (which was caught up in the oversupply furore some weeks ago) is now trading at around 4%.

The bond markets, ever perceptive, are signalling a narrative of their own. The rapid adjustment of interest rates post the Fed’s short-end curve manipulation cessation reflects a troubling sign. Rates, fundamentally tethered to growth and inflation outlooks, have taken a nosedive.

Yet, low rates rarely herald favourable long-term growth prospects.

As far as long run growth potential goes, low rates are not a good sign.

This isn’t merely a US phenomenon; it's a global bond market rally. Rates in Europe and Japan are sliding too, despite official statements suggesting otherwise. Although Lagarde announced that they are not thinking about rate cuts, the market knows better. And, such a collective downward trend in rates hints at unsettling growth expectations on a broader scale.

Has the anticipated Soft Landing Materialized?

The burning question emerges: Has the anticipated soft landing materialized? While the bond markets are pricing in fundamentals, stock markets toasted the idea of a smooth economic descent.

But, the Fed's acknowledgment of substantial economic activity slowdown contradicts the celebratory mood. The consecutive months of stagnant CPI imply disinflation's arrival. However, this slowdown hasn't been coupled with a surge in unemployment. Moreover, by the Fed’s own projections, personal consumption expenditures price index will finally reach its 2% target in 2026, leaving room for debate about the necessity of imminent rate cuts.

Could it be that Chairman Powell and the Fed are realizing the markets have taken the lead, considering their inherently backward-looking nature? Perhaps the Fed senses a risk beyond a soft landing hence justifying pre-emptive rate cuts as a protective measure?

What Does This Mean for Investors?

The Fed has clearly gone softer on their inflation mandate with their prediction that the core personal consumption expenditures price index will finally reach its 2% target in 2026.

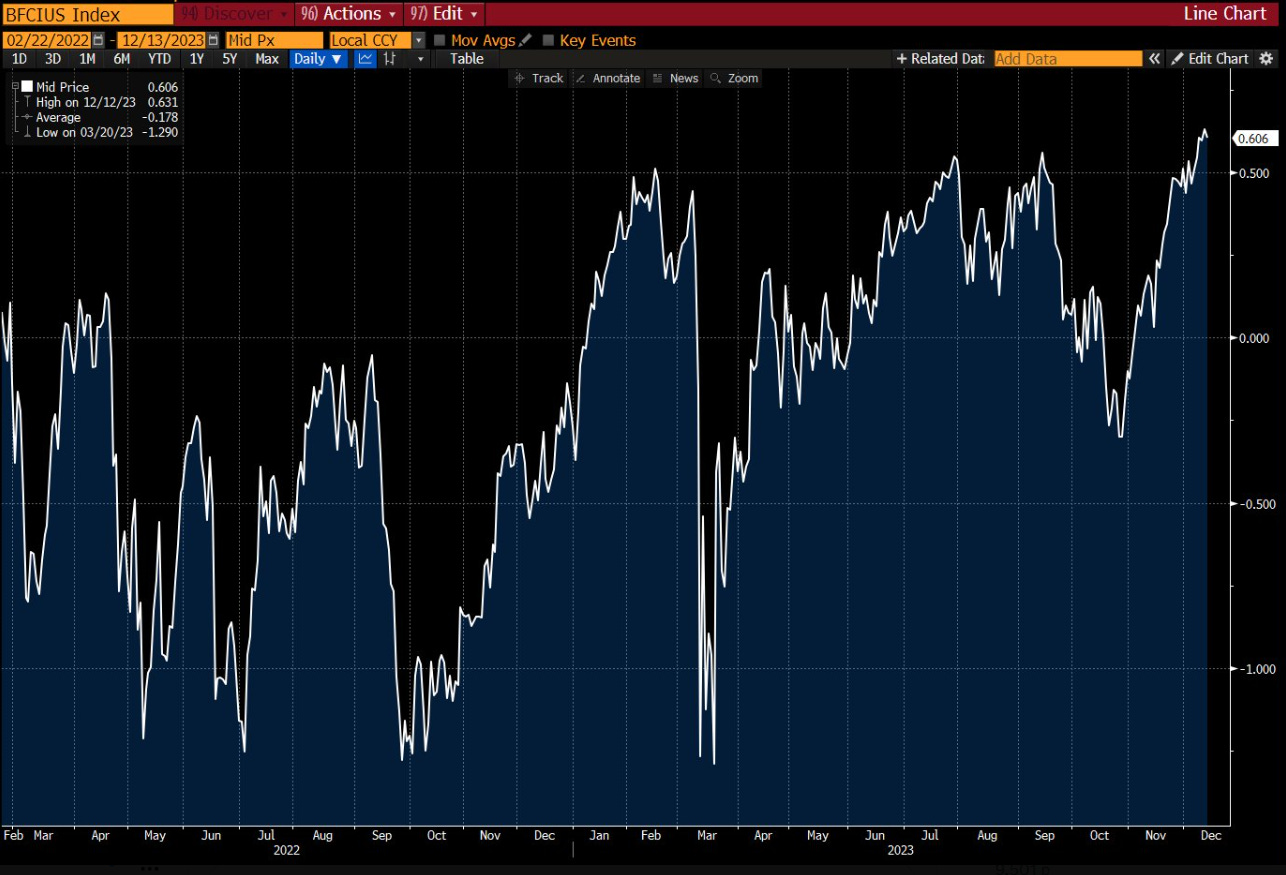

Lisa Abramowicz from Bloomberg highlighted that U.S. financial conditions are the most accommodative they've been since the Fed started hiking rates last year according to Bloomberg.

With the Fed having clearly gone soft on their inflation mandate, a concerning risk emerges: the risk is that we could suddenly find ourselves in an environment in 2024 where the economy starts to overheat triggered by substantial market rallies. If this occurs, the Fed may be compelled to apply tightening measures. But that’s a scenario we will have to revisit at a later stage.

Cash

For now, cash investors should seize the moment to rebalance. Markets have already adjusted expectations for rate cuts. Hence, it’s an opportune time to shift cash from money markets into bonds to lock in higher yields. A short maturity strategy can offer an opportunity to lock in compelling positive yield levels available now with relative lower risk and high visibility on returns.

Fixed Income

Fixed-income investors, however, should exercise caution. While a dovish Fed typically triggers a bond rally in duration, the confluence of factors—lower yields, higher equity prices, increased government and Capex spending, among others—may dampen bond attractiveness despite falling inflation.

Equities

In the equities realm, the recent post-Fed stock rally has brought festive cheer, and the momentum should persist through to year end. Nonetheless, selectivity will be crucial as we step into 2024.

Liquid Alternatives and Absolute Return Strategies for Diversification

And finally, as we head into 2024, the levels of uncertainty will continue to remain elevated and that could lead to a situation where traditional asset classes once again correlate on the downside. Absolute return strategies and alternative investments in hedge funds can offer a very useful source of diversification.

Have a great week ahead!

Please Like and Subscribe if you enjoyed this post. It helps me get the word out about my newsletter, thank you!

***Disclaimer***

All opinions are mine and personal. Please do not construe any of my posts as investment advice. I do not provide any buying or selling recommendations, nor offer any investment advice. You are advised to conduct your own research and due diligence when making financial and investment decisions.